Homeowners Insurance Generating Homeowners Insurance Leads With Life Saver Leads

Homeowners insurance is a crucial aspect of property ownership that provides financial protection against various types of damages to one's home and personal property. This type of insurance can be tremendously beneficial for homeowners, offering peace of mind and financial security in times of crisis. Below, we will delve into the fundamental aspects of homeowners insurance, exploring its benefits, common types of coverage, factors affecting premiums, and key considerations for selecting a policy.

What is Homeowners Insurance?

Homeowners insurance is a form of property insurance that covers private homes. It provides a combination of coverage for the structure of the home itself, liability protection, and additional living expenses associated with loss or damages caused by covered events.

Benefits of Homeowners Insurance

Here are some key benefits of having homeowners insurance:

- Protection Against Financial Loss: In case of damage due to fire, theft, or natural disasters, homeowners insurance can cover repair costs, mitigating the financial burden on the homeowner.

- Liability Coverage: If someone is injured on your property, homeowners insurance can help cover medical bills and legal fees resulting from the incident.

- Peace of Mind: Knowing that your home and belongings are protected can provide significant peace of mind, allowing you to focus on other important aspects of life.

Common Types of Coverage

Homeowners insurance typically includes several types of coverage, including:

- Dwelling Coverage: Protection for the structure of your home, including walls, roof, and other permanent features.

- Personal Property Coverage: Covers the personal belongings inside the home, such as furniture, electronics, and clothing, against covered risks.

- Liability Protection: Safeguards homeowners against legal expenses and claims due to injuries or damages that occur on their property.

- Loss of Use Coverage: Covers additional living expenses if the home becomes uninhabitable due to a covered loss, such as temporary housing costs.

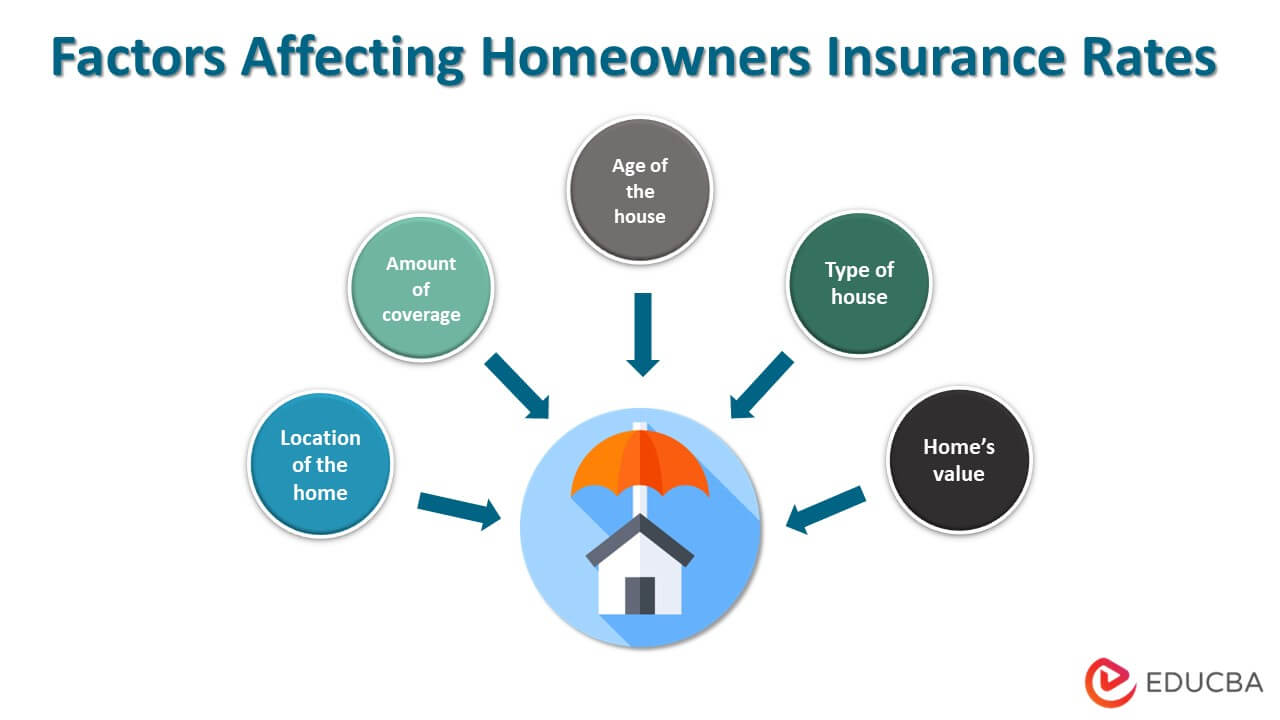

Factors Affecting Homeowners Insurance Premiums

Various factors can influence homeowners insurance premiums, including:

- Location: Homes in areas prone to natural disasters, such as floods or earthquakes, generally incur higher premiums.

- Home's Age and Condition: Older homes may have higher premiums due to potentially outdated structures and systems, while newer homes may benefit from lower rates.

- Coverage Amount: The more extensive the coverage, the higher the premium. Homeowners must balance adequate coverage with affordability.

- Your Credit Score: Insurers often use credit scores to determine risk; better credit scores can lead to lower premiums.

Key Considerations When Selecting a Policy

When purchasing homeowners insurance, it's important to consider the following:

- Coverage Limits: Ensure your policy offers sufficient coverage for both dwelling and personal property.

- Deductibles: Understand the deductibles you are willing to pay in the event of a claim. Higher deductibles may lower premiums but could increase out-of-pocket expenses when filing a claim.

- Exclusions: Be aware of what is not covered by your policy, such as certain types of water damage or natural disasters, and consider supplemental insurance if needed.

- Comparative Quotes: Obtain quotes from multiple insurance providers to find a policy that meets your coverage needs and budget.

Homeowners insurance is not only a safeguard for your property but also an essential component of responsible homeownership. Understanding its intricacies can empower you to make informed decisions that best protect your assets.

1. What are the primary distinctions between different types of homeowners insurance policies?

The primary distinctions between different types of homeowners insurance policies lie in their coverage levels and the specific protections they offer. The most common types—HO-1 (basic form), HO-2 (broad form), HO-3 (special form), and HO-5 (comprehensive form)—vary in terms of what perils are covered and whether personal property is insured on an actual cash value or replacement cost basis. HO-3 is the most frequently chosen policy as it generally covers the dwelling on an open-peril basis and personal belongings on a named-peril basis, providing a balanced, comprehensive option for homeowners.

2. How does homeowners insurance protect against liability claims?

Homeowners insurance protects against liability claims by offering coverage for legal expenses and compensation for damages resulting from injuries or accidents that occur on the homeowner's property. This protection typically includes scenarios like slip and fall incidents, pet bites, or damages caused by structural failure. The liability coverage provides financial support for medical costs or legal fees, ensuring that homeowners are not solely responsible for significant out-of-pocket expenses that arise from such claims.

3. In what ways can increasing home security influence homeowners insurance premiums?

Increasing home security can lower homeowners insurance premiums by demonstrating to insurers that the risk of property damage or theft is reduced. Homeowners who invest in security systems, deadbolts, smoke detectors, and other protective measures may qualify for discounts because these enhancements minimize the likelihood of claims. Insurers recognize the reduced risk associated with secure properties, which can lead to a more favorable rate for the policyholder.